A common rationale for owning Bitcoin is that its logarithmic money supply makes it a good store-of-value (SOV). Like precious metals or rare paintings stored in Swiss vaults, the scarcity of those coins will ensure that they at least keep their value.

By itself, this argument is hopelessly naive, as there is nothing scarce about a cryptocurrency with a fixed terminal money supply; anyone can (and a great many have) fork Bitcoin and create another such currency, so the total supply of such coins is potentially unlimited. But it could be replied that there are powerful network effects here, that the demand for digital SOV will coordinate around just one or two “crypto gold” stocks. In a previous post I’ve argued that the continuous hashing costs required to make the p2p secure would indeed imply such a network effect, but that the inability of log coin supply to finance these hashing costs out of seigniorage after the money supply stops growing casts doubts about the sustainability of this spontaneous digital gold enterprise.

A more sophisticated defence of Bitcoin’s valuation goes like this. Bitcoin is great SOV not just because of its limited supply and those hashing cost network effects. It’s a great SOV because in future more and more people will use it as a medium-of-exchange (MOE). As the volume of bitcoin transactions increases, so will the demand to hold bitcoin balances for the purpose of making transactions in goods and services. But a total of only 21 million bitcoins will ever be produced, so the price of a bitcoin must reflect the ratio of expected future MOE money demand to 21 million. The price of Bitcoin, one might argue, is the market’s prediction of the long-term growth rate of bitcoin transaction demand.

So let’s set aside the theoretical objection to this thesis and look at it empirically. Is there evidence of transaction growth to date that would rationalise Bitcoin’s valuation if we extrapolate recent tx growth?

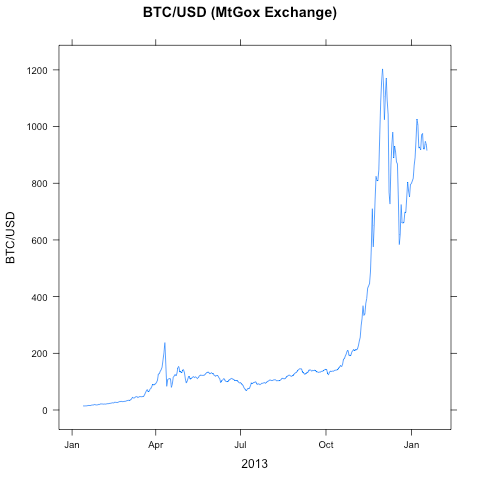

Here are the daily transaction volumes and BTC/USD fx volumes aggregated from the main exchanges.

Just eyeballing this chart, it looks to me like there is very little transaction growth except for the period at the end of the first and fourth quarters, when there were dramatic revaluations in the exchange rate. And the explanation that leaps to my mind for those spikes in tx volume is that it’s coming from the settlement of fx trades for buy-and-hold positions in bitcoin, and a good deal of Chinese evasion of capital controls via CNY –> BTC –> USD, GBP, EUR..

But a more bullish story could be told. The revaluation of Bitcoin might have had a large wealth effect, with early Bitcoin adopters spending some of their increasingly dear hoard on weed and alpaca socks, and the revaluation was itself due in large part to newcomers buying bitcoin for the purpose of buying stuff with it.

Transactions on the blockchain that are settling an fx trade should be excluded from our calculation of bitcoin transaction growth. For every buy, there is a sell, so these transactions cannot represent new transaction demand by definition.

The data series used in these charts come from blockchain.info, and unfortunately, it only has fx volume for BTC/USD. Ideally, we’d want the volume figures for BTC vs EUR, GBP, CNY, JPY, and others so that we could add them all up and subtract total fx volume from the transaction series to get a truer picture of underlying transaction growth. If anyone can point me to where I can get those data easily, I’ll run the analysis.

Until then, here are monthly Bitcoin total transaction and BTC/USD trade month-on-month volume growth figures (in USD).

yearmm tx fx 201301 0.554 1.105 201302 0.620 0.673 201303 1.304 2.188 201304 1.765 3.349 201305 -0.388 -0.580 201306 -0.318 -0.521 201307 0.265 -0.183 201308 -0.161 -0.323 201309 0.112 -0.109 201310 0.681 1.196 201311 3.847 4.150 201312 -0.015 0.207 Average Monthly Growth (2013) tx fx 0.413 0.418

These data are not conclusive. You could argue that the roughly 40% monthly tx growth is impressive evidence of underlying transaction growth. Or, you could interpret the roughly identical growth rates of tx and fx volume, and their high monthly correlation, as evidence that most of the tx growth is due to fx settlements. We need a complete fx volume series to disambiguate the data. When we do that, my bets are that monthly tx growth is under 20%.

I will happily accept you guesstimate of 20% tx growth … that is still an incredible compound growth rate. An business trying to establish a new product would be ecstatic with that growth rate.

“By itself, this argument is hopelessly naive, as there is nothing scarce about a cryptocurrency with a fixed terminal money supply; anyone can (and a great many have) fork Bitcoin and create another such currency, so the total supply of such coins is potentially unlimited.”

Only if your fork is accepted by a large enough user base/companies/exchanges. E.g., Overstock only accepts BTC but not Litecoins, Primecoins, etc.

True, that’s almost 800% on a compound annualised basis. But everything is relative. BTC/USD in 2013 appreciated by around 5,500%, and the idea is to relate one to the other. Tx volume in 2013 was about 15bio USD (and that’s including fx settlements), and Bitcoin monetary base is about 11bio. That’s a money velocity–the number of times that a coin changes hands over the year–of only 1.3. If those bitcoin are in some future time to be used primarily as an MOE, we’d expect to see velocity much higher than that. So I’d argue that tx growth needs to be allot higher to rationalise BTC/USD on the thesis that it’s on its way to becoming a widely used MOE.

“By itself, this argument is hopelessly naive, as there is nothing scarce about a cryptocurrency with a fixed terminal money supply; anyone can (and a great many have) fork Bitcoin and create another such currency, so the total supply of such coins is potentially unlimited.”

It’s not hopelessly naive to say it is scarce, it’s an absolute truth. What is naive is to think that just because something is scarce, it has to be valuable. Scarcity would appear to be a necessary condition, but not a sufficient one. But that’s a different argument.

Looking at transaction volume is simplistic, since we don’t know how many of these transactions correspond to payments for real world goods and services. There’s also no easy way to identify the amounts involved because bitcoins have to be spent in their entirety with any excess amount returned as change. Unfortunately it’s not easy to tell which of the outputs is change, as it’s generally not sent back to the originating address (or addresses).

People have tried to devise all sorts of proxies for the actual dollar volume of Bitcoin transactions, but there are no good answers yet. Looking at payments processed by Bitpay and Coinbase would be a better metric.

And of course, we do see that more and more companies are starting to accept Bitcoin, including semi-well-known ones such as Overstock, Zynga, and TigerDirect. Internet porn sites also seem poised to embrace Bitcoin, porn.com already accepts it, Wicked has annouced it, Naughty America is rolling it out and Verotel, a payment processor, is rolling it out for all its customers.

I know about the change issue, but have not looked into how blockchain.info tries to adjust for it, I just know that the series that I used from them does. Do you know if Bitpay and Coinbase publish their tx volume figures? At any rate, we can certainly make some upper-bound estimates from these data.

Apart from the occasional press release, I don’t think this data is public.

http://www.businesswire.com/news/home/20131211005909/en/BitPay-Exceeds-100000000-Bitcoin-Transactions-Processed#.UuUmPbSvmpo

You can pull historical price and volume data on many, many exchanges all over the world from https://bitcoinaverage.com, which nicely aggregates them by currency and even provides cross rates.

Great thanks, I’ll check it out.

Pingback: Can we value Bitcoin? | Crypto News Desk

Pingback: Can we value Bitcoin? – ABQ Crypto