In a post a few weeks ago I wrote:

A more sophisticated defence of Bitcoin’s valuation goes like this. Bitcoin is great SOV not just because of its limited supply and those hashing cost network effects. It’s a great SOV because in future more and more people will use it as a medium-of-exchange (MOE). As the volume of bitcoin transactions increases, so will the demand to hold bitcoin balances for the purpose of making transactions in goods and services. But a total of only 21 million bitcoins will ever be produced, so the price of a bitcoin must reflect the ratio of expected future MOE money demand to 21 million. The price of Bitcoin, one might argue, is the market’s prediction of the long-term growth rate of bitcoin transaction demand.

Now, on Twitter today Marc Andreessen, links to Fortune article citing Stanford economist Susan Athey, who apparently makes an argument virtually identical to the above:

An anonymous viral email circulating among bitcoin watchers and partisans lays out a few simple hypothetical usage and adoption scenarios, and their consequences for bitcoin’s price. If Amazon.com adopted bitcoin for all payments, its volume of $38 billion, divided by a supply of (at the time of the email’s writing) about 7 million bitcoin, would make each bitcoin worth $5,400. If $300 billion in international remittance was conducted in bitcoin, that volume alone would push the price to $42,000. Adding these, along with online poker and gas station transactions, would lead to a total transaction volume of $602 billion – and a bitcoin, even at today’s expanded supply of 12 million coins, worth $50,000.

“Those numbers are good ones to start with. In some sense, that’s like a maximum,” says Susan Athey, a professor of economics at the Stanford Graduate School of Business who has been studying bitcoin. Few would realistically argue that bitcoin will service 100% of even these silos in the near term, but the volume/supply ratio is the starting point for understanding bitcoin price – as more consumers or organizations choose to use bitcoin, increased volume will drive the price up.

Building from that basic formula, Athey adds a variety of variables to build an analytic framework. The first is velocity – how frequently a bitcoin can be spent. Because bitcoin, unlike paper money, is very low-friction, there’s the possibility of a very high-velocity bitcoin, if, for example, vendors or traders only held bitcoin very briefly, cashing it in and out to government currencies on either end of transfers. That, Athey says, would allow a small volume of bitcoin to process a large volume of payments, keeping the price of bitcoin relatively low.

I’m not privy to this exchange, so I don’t know how much of this argument is attributed to Athey and how much is the Fortune journalist’s own thinking. A bit of Googling turned up this interview with Athey in November of last year:

What do you think about the bitcoin price increases recently? Well, if you expect the volume of transactions to grow a lot, then the exchange rate from dollars to bitcoins has to grow too, because each bitcoin can only be used so many times per day. The market value of all bitcoins has to be enough to support transaction volume. You could interpret the price increases as reflecting increased optimism about the future volume of transactions, driven by China implicitly signaling that it will allow bitcoins to be used for commerce there.

As I pointed out in my previous post, this is a more sophisticated rationalisation of a Bitcoin’s valuation than one usually reads. As a cryptocurrency pays no income, the only way to value it fundamentally is in terms of expected future cryptomoney demand (uncertain) in relation to its future supply (deterministic and completely predictable in Bitcoin). By “cryptomoney demand” we mean: crypto coin balances held for the purpose of facilitating transactions in that coin.

Money demand is proportional to the level of transaction volume if velocity–the number of times the coin supply changes hands over the period–is stable. So, if we can make that assumption of stable velocity, the price of Bitcoin today should reflect expectations of future bitcoin transaction volume. Let  be some future time when the growth rate of transaction volume

be some future time when the growth rate of transaction volume  levels out and let

levels out and let  be the velocity at time , and

be the velocity at time , and  is the supply of bitcoin:

is the supply of bitcoin:

The calculation cited above arriving at that BTC = $50,000 is implicitly assuming a money velocity of 1, which goes against the Silicon Valley vision of a Bitcoin-as-payments unit that people swap in and out of via intermediaries like Coinbase and BitPay. In that scenario, velocity will be very high.

Here is a back-of-envelope valuation. Let’s say that represents year 2024 and that bitcoin transaction growth levels out in about 10yrs time. Now, let’s fix an assumption of velocity at that time. The money velocity of USD M1 is about 7, so I would guess that Bitcoin velocity will be rather higher than that. Let’s just say, arbitrarily, that Bitcoin velocity will be 10X USD money velocity. So BTC = $650, = 70, and = 20 million, making = $910 billion, almost 6% of the US economy.

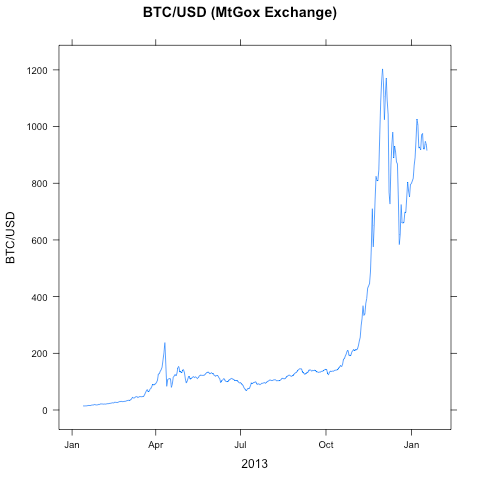

The result isn’t totally crazy. Here are the blockchain transaction volume figures for the last four years, converted into USD values at the time of transaction (as calculated by blockchain.info):

year volume growth

2010 985,887 0%

2011 418,050,216 42,303%

2012 601,415,369 44%

2013 15,216,615,077 2,430%

Much of that volume will be FX settlements and payments between addresses controlled by a single entity, and those volumes shouldn’t be included in the analysis. How much is difficult to estimate (something that we’ll look into in a future post), but let’s say that half of that volume should be excluded, so the current base is 7.6 billion per-year. Annual volume of 910 billion annual in a decade’s time is a bit over 60% compounded growth per year. In light of recent history, the result is conservative!

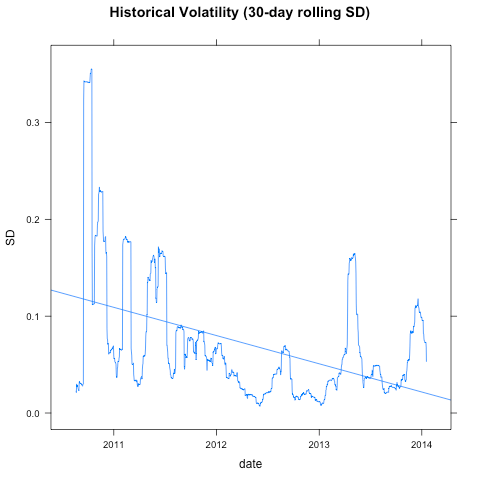

The problem with this sort of valuation analysis is that the inputs and are entirely speculative. Assumptions, assumptions, assumptions. You can plug-in anything you like. It’s like valuing a new business.. but worse. In Bitcoin the is basically fixed in future horizons (never more than 21 million), so any change in the market’s assumptions translates into changes in the exchange rate. Bitcoin translates that uncertainty about its future prospects into present exchange rate volatility. And that exchange rate volatility dampens demand today for using bitcoin as a medium-of-exchange, undermining the very assumptions behind its current valuation. To me Bitcoin–not cryptocurrency in general, but Bitcoin–is like one of those M.C. Escher drawings, where the impossible looks deceptively plausible.

The Bitcoin-as-payments people will reply that the volatility doesn’t matter, that I’m wrong in saying that the volatility undermines the transactional demand for bitcoin. Here’s a recent claim by Andreessen:

The criticism that merchants will not accept Bitcoin because of its volatility is also incorrect. Bitcoin can be used entirely as a payment system; merchants do not need to hold any Bitcoin currency or be exposed to Bitcoin volatility at any time. Any consumer or merchant can trade in and out of Bitcoin and other currencies any time they want.

Athey qualifies this position a little (from the same interview above):

What about the extreme volatility? Volatility is bad because it increases frictions—if I just want to send you $100, the exchange rate might change between when I buy the bitcoins and send them to you, and when you receive and cash them out. That creates risk and frictions. But the level of the exchange rate is irrelevant for the efficiency of the payment rail—if I knew it would be $1000/bitcoin all day long, or $100/bitcoin, either way I can buy bitcoins, send them to you, and you can sell them, while avoiding paying exorbitant bank fees. You still incur some fees when getting money in and out, but those are relatively low and should fall over time with competition.

But the irreducible component of the costs facing those merchants Andreessen speaks about are those very “risks and frictions”, they make the price of offloading that volatility to someone else. Competition will not reduce those costs any more than competition among options dealers will reduce the price of a put on the S&P 500.

Is the 1% fee that Coinbase charges for the service of offloading exchange rate volatility sufficient to cover their cost of hedging a coin whose USD volatility is more than 7 times that of the stock market? There are a smart bunch of people behind that company, so I’m reluctant to second-guess the business model. But I feel I must.. and may do so in detail in a future post.

The implicit assumption behind the comments of Andreessen and Athey is that Bitcoin’s money velocity can be arbitrarily large, a hot potato that gets passed around so quickly that the volatility of the coin can be made negligible to the party using it as medium-of-exchange. But the Bitcoin protocol itself places a lower limit on the speed of transaction confirmations, placing an upper limit on Bitcoin’s velocity. Whatever that velocity turns out to be, the interval between time coin received and time coin paid will impose an irreducible risk on the party who wishes to use Bitcoin to make payments. A risk that is costly to layoff to someone else.

But I am a believer in cryptocurrency, I would just prefer to back a cryptocurrency where whose supply was more responsive to its demand, where  is a function of

is a function of  , or a function of the exchange rate itself. This can be done in an entirely trustless way, and such a coin is likely to have a much more stable exchange rate and be a better medium-of-exchange.

, or a function of the exchange rate itself. This can be done in an entirely trustless way, and such a coin is likely to have a much more stable exchange rate and be a better medium-of-exchange.

and you get a quarterly money velocity for bitcoin of just under 7.

and you get a quarterly money velocity for bitcoin of just under 7. is biased upwards.

is biased upwards. , where B is the address balance after the coins are paid in. Whenever coins are spent by an address, its dormancy is unchanged (dormancy is a property of the remaining coins). But spends reduce the address balance, so subsequent coins received will reduce dormancy even more.

, where B is the address balance after the coins are paid in. Whenever coins are spent by an address, its dormancy is unchanged (dormancy is a property of the remaining coins). But spends reduce the address balance, so subsequent coins received will reduce dormancy even more.